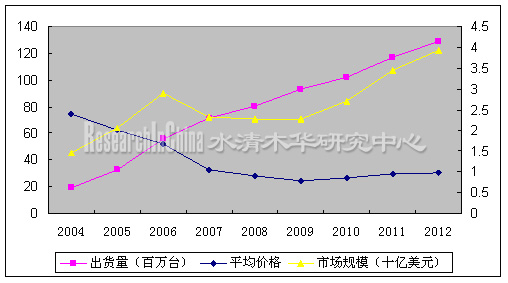

2004-2012年全球数字电视出货量与数字电视IC市场规模统计及预测

注一:这里的市场规模指数字电视中所有IC元件的市场规模、包括内存、接口、MCU和音频部门,某些非专业调研机构将液晶和等离子电视的驱动IC也算进数字电视IC,实际电视机厂家采购的液晶面板和等离子面板中早已包含了驱动IC,因此不能算数字电视IC。

注二:这里的数字电视指的是集成型数字电视,不需要附加任何设备就可以接收数字电视,因此比大多数研究结构算的数据要小。

CRT时代,数字电视与模拟电视最大的区别是数字电视多数字电视解调芯片、MPEG-2解码芯片和视频DAC。而平板电视时代,情况有了变化,平板电视主要是液晶电视和等离子电视。这些显示元件都是数字信号显示元件,也就是说液晶面板和等离子面板可以直接对应数字信号,而显像管是无法对应数字信号的。平板电视时代,数字电视和模拟电视的差别在于数字电视多数字电视解调芯片、MPEG-2解码芯片,视频DAC不需要了。不过考虑到还有很多模拟视频设备,数字电视又多了一个视频ADC。

目前数字电视里主要芯片有信号解调芯片、视频控制芯片、MPEG-2解码芯片、视频处理芯片、HDMI接口芯片、音频处理与音频放大芯片,也就是大约7片IC。高级的超过37英寸的数字电视多采用分离型设计,至少有7片IC。有时候会再多一片MCU来弥补视频控制IC的性能。中高档的32-37英寸的数字电视通常会将视频控制和视频处理集成在一片芯片上。20-32英寸的数字电视通常会将视频控制芯片、MPEG-2解码芯片、视频处理芯片集成在一起,有时也包括HDMI接口。而未来的发展趋势是除高级的超过37英寸的数字电视外,其余尺寸的电视都会采用高度集成的单芯片设计,信号解调芯片、视频控制芯片、MPEG-2解码芯片、视频处理芯片、HDMI接口芯片和音频处理都会集成在一片芯片上。也就是SoC。单片设计大幅度降低数字电视的半导体成本和设计难度。

这场SoC潮流带来的是数字电视IC界的腥风血雨,台湾厂家则是这场血战的始作俑者。联发科和晨星半导体最早开打。本来不计调谐器,解调器、视频处理与控制和MPEG-2解码IC三片关键IC报价在2006年大约为40-50美元。台湾厂家在2007初直接报价就是20美元,量大价格还可以再低,2007年底则低于15美元。欧美厂家立刻被打得头破血流,亏损惨重。

第一个倒霉的是Genesis,从2006财年起,该公司开始走下坡路,收入和毛利率快速下滑。2008年财年上半年该公司收入1亿美元,运营亏损2160万美元。无论收入和利润都比去年同期大幅度下滑。不过Genesis毕竟曾经是全球第一的液晶电视控制IC厂家,技术实力雄厚;亟需要后段技术配合的半导体巨头意法半导体在2007年底以3.36亿美元的高价买下Genesis。所有人都认为这个价格太高了,也许只有意法半导体认为不高。

第二个倒霉的是Pixelworks,该公司2005年电视领域内的收入有近9000万美元,而2007年萎缩到只有1980万美元。第三个倒霉的是欧洲企业。Micronas是全球最大的数字电视音频IC厂家,总部在瑞士,2006年亏损1700万瑞士克朗,2007年亏损幅度狂增30倍,达到5.43亿瑞士克朗,也就是约5.43亿美元,差不多要破产了。第四个倒霉的是AMD/ATI,ATI走超高端路线,受的影响最小。不过即便是三星也禁不住联发科低价的诱惑,AMD/ATI的消费类电子部门第一次出现亏损。马上要倒霉的是泰鼎,依靠索尼、三星这样的强力合作伙伴,泰鼎的日子还算不错。但是泰鼎2008财年预计收入增长只有7%,而2007财年的收入增长为58%。快速增长的势头已经被台湾厂家遏制。

全球电视市场主要厂家有索尼、松下、夏普、三星、LG、飞利浦、TTE。CRT时代,索尼是最顶级电视的代名词,所用的IC都是自己开发。平板时代,索尼落伍了,索尼开始以低价竞争,索尼的电视用IC都开始从外采购。高端的有AMD/ATI和泰鼎支持,低端则有NXP支持,用三星的屏加上华裔厂家泰鼎的IC,这个索尼谁都可以做到。三星和夏普则是泰鼎的忠实顾客。LG则依靠Genesis,泰鼎和Broadcom。飞利浦自然是靠NXP。唯有松下,令人肃然起敬,所有IC都自己开开发。而中国厂家则迫不及待地投入联发科和晨星的怀抱。康佳几乎所有的平板电视都是晨星的IC,TTE、长虹则喜欢联发科。联发科的价格稍高,用晨星的产品还是更多。晨星占中国平板电视65%的市场份额,这家从不公布财务报表却股价最高的台湾公司分明就是联发科第二。联发科目前主要还是依靠台湾的电视代工厂家进军美国市场,远不如晨星开拓大陆市场来得顺利,这一次联发科终于遇到了最强的对手。

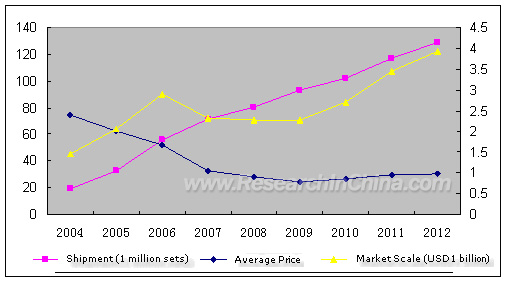

Statistics and Forecast of Global DTV Shipment and DTV IC Market Scale, 2004-2012

Note:

The market scale here refers to all IC components of DTV, including EMS memory, interface, MCU and audio frequency. Some unprofessional research organizations also count drive IC of LCD TV and plasma TV into DTV IC, but in reality it should not be counted, due to the fact that while producers buy liquid crystal panel and plasma panel, driver IC is already included in the panels. The digital TV here refers to integrated DTV, which can receive digital TV programs without any extra device. Therefore, the statistics here are smaller than those of the majority of research organizations.

In the era of CRT, the largest difference between digital TV and analog TV is digital TV has digital TV decode chip, MPEG-2 decode chip and video DAC. But in the era of flat panel TV, composed mainly of LCD TV and plasma TV, the situation has changed. All these display components are digital signal ones, indicating that the liquid crystal panel and plasma panel can correspond the digital signal directly, while the picture tube can not correspond digital signal. In the era of flat panel TV, the difference between digital TV and analog TV is digital TV has digital TV decode chip, MPEG-2 decode chip, so video DAC is not needed. But considering many analog video equipment, digital TV has a video ADC.

Currently, digital TV mainly has about seven chips, like Signal demodulator chip, video-control chip, MPEG-2 decode chip, video processing chip, HDMI interface chip, audio frequency treatment chip and audio frequency amplification chip. High-end DTVs with more than 37 inches in size mainly adopt separation design, requiring at least seven chips, and sometimes one more MCU chip is needed to make up for the performance of video-control IC. Medium- and high-level DTVs with 32-37-inch sizes usually integrates video control chip and video processing chip into a single chip, while DTVs with 20-32 inches in size usually integrates video-control chip, MPEG-2 decode chip and video processing chip into one single chip, sometimes HDMI interface chip is included. The future development trend is except high-end DTVs with more than 37 inches in size, the other sizes of TV will all adopt highly integrated single chip design, which integrates signal demodulator chip, video-control chip, MPEG-2 decode chip, video processing chip, HDMI interface chip and audio frequency processing chip into a single chip, namely SoC. The single chip design has sharply decreased the cost of DTV semiconductor and design difficulty.

The SoC trend has brought about a serious competition to the DTV industry. Media Tek and MStar Semiconductor initially launched the price war. In 2006, the prices of a chipset, including demodulator chip, video processing and controller chip and MPEG-2 decode chip but excluding tuner chip, were around US$40-US$50. In early 2007, the price dropped to US$20, which could be lower given a large order, and it fell to below US$15 at the end of 2007. The cut-throat competition was a heavy toll to the European and U.S. companies suffering huge losses.

Genesis was the first one to be beaten. From fiscal year 2006 onwards, the company was on the downward trend with its revenue and gross profit margin declining rapidly. Its revenue in the first half of fiscal year 2007 was US$100 million and its operation loss amounted to US$21.6 million. Both the revenue and profit had a big fall compared to the same period of the previous year. But Genesis as the former first LCD TV control IC manufacturer in the world had a powerful strength in technology, which made ST take over the company at the price of US$336 million at the end of 2007.

Pixelworks was the second unfortunate fellow, whose revenue in TV field amounted to US$90 million in 2005 and shrank to only US$19.8 million in 2007. The European manufacturers also suffered losses in tandem with U.S. companies. Micronas, the world’s largest DTV audio frequency IC manufacturer with its headoffice based in Switzerland, had a loss of CHF17 million in 2006, and its loss soared to CHF543 million in 2007, which has placed the company on the brink of bankruptcy. AMD/ATI was the next. The consumer electronics division of AMD/ATI had its first loss, while ATI with its target pinpointing at the ultra high-end produces suffered the least impact. Trident, relying on the powerful partners like Sony and Samsung, had a good performance, but it is also facing a tough time ahead. Its revenue in fiscal year 2008 is expected to grow 7% only, while the growth rate was 58% in fiscal year 2007. The rapid growth has been restricted by the manufacturers in Taiwan.

The global TV market has mainly the following manufacturers, like Sony, Panasonic, Sharp, Samsung, LG, Philip and TTE. In the era of CRT, Sony was the top TV brand with all its IC developed independently. In the era of panel TV, Sony lagged behind. It started to compete with low prices with all its IC for TV outsourced. Samsung and Sharp are the loyal clients of Trident, while LG depends on Genesis, Trident and Broadcom. Philip relies on NXP. Only Panasonic develops all its IC independently. The manufacturers in Mainland China are eager to adopt the products of Media Tek and MStar Semiconductor. Nearly all the flat panel TVs of Konka adopts MStar Semiconductor’s IC, while TTE and Changhong prefer Media Tek. However, MStar Semiconductor enjoys 65% of the flat panel TV market share in Mainland China. Currently, Media Tek is entering the U.S. market through the TV OEMs in Taiwan, but the progress is not as smooth as MStar Semiconductor’s exploitation in mainland market.

第一章 数字电视概述

1.1 数字电视概念

1.1.1 数字电视有哪些优势和特点?

1.1.2 数字电视地面传输标准

1.2 数字电视芯片简介

1.2.1 数字液晶电视设计

第二章:全球电视机市场与产业简介

2.1、全球电视机市场发展趋势

2.2、全球液晶电视产业概况

2.2.1、液晶面板产业概况

2.2.2、液晶电视市场与发展趋势

2.2.3、 台湾地区LCD TV组装厂

第三章、数字电视IC市场现状与未来

第四章:先进电视机实例设计分析

4.1、三星LN-T4665F

4.2、三星HPT5064

4.3、康佳

4.4、LG 26LC2D

4.5、VIZIO L37HDTV

第五章:先进电视IC厂家研究

5.1、TRIDENT

5.2、GENESIS(ST)

5.3、ZORAN

5.4、晨星半导体

5.5、联发科

5.6、其乐达

5.7、MICROTUNE

5.8、三星

5.9、MICRONAS

5.10、NXP

5.11、SILICONIMAGE

5.12、BRODCOM

5.13、AMD/ATI

5.14、成都威斯达

5.15、瑞萨

5.16、Pixelworks

1. Overview of DTV

1.1 Definition

1.1.1 Advantages and Characteristics

1.1.2 Terrestrial Transmission Standard

1.2 DTV IC

1.2.1 Design of Digital LCD TV

2. Global TV Market and TV Industry

2.1 Development Trend

2.2 Industry Overview

2.2.1 LCD Panel Industry

2.2.2 LCD TV Market and Its Development

2.2.3 LCD TV Assembly Plants in Taiwan

3. Status Quo and Future of DTV IC Market

4. Examples of Advanced TV Design

4.1 Samsung LN-T4665F

4.2 Samsung HPT5064

4.3 Konka

4.4 LG 26LC2D

4.5 VIZIO L37HDTV

5. Advanced TV IC Manufacturers

5.1 TRIDENT

5.2 GENESIS (ST)

5.3 ZORAN

5.4 MStar Semiconductor

5.5 Media Tek

5.6 Cheertek

5.7 MICROTUNE

5.8 Samsung

5.9 MICRONAS

5.10 NXP

5.11 SILICONIMAGE

5.12 BRODCOM

5.13 AMD/ATI

5.14 Chengdu West Star

5.15 Renesas

5.16 Pixelworks