|

报告导航:研究报告—

制造业—化工

|

|

2007-2008年中国煤焦化上市公司研究报告 |

|

字数:2.0万 |

页数:51 |

图表数:54 |

|

中文电子版:5000元 |

中文纸版:2500元 |

中文(电子+纸)版:5500元 |

|

英文电子版:1400美元 |

英文纸版:1300美元 |

英文(电子+纸)版:1700美元 |

|

编号:EY002

|

发布日期:2008-04 |

附件:下载 |

|

|

|

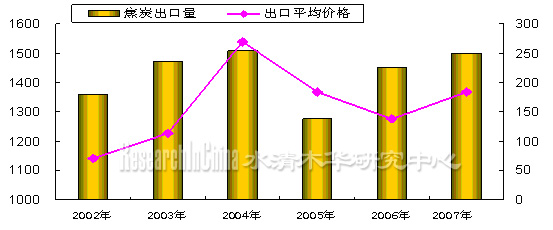

煤焦化是发展最成熟、最具代表性的煤化工产业,也是冶金工业的辅助产业。中国炼焦技术已进入世界先进行列,成为世界焦炭生产、消费及贸易第一大国。近年来,煤焦化市场逐步复苏,带来产品价格的持续上涨,从行业周期的角度来看,我们认为焦炭行业正处于行业景气提升的阶段。

焦炭出口平均价格自2005年下半年大幅度下跌以来,在2006年开始止跌回升,2006年年内最大涨幅曾经达到过33美元/吨。进入2007年以来更是逐月环比上涨,在涨幅最大的第三季度平均价格达到了203美元/吨,比上年同期144美元/吨,累计上涨了近60美元/吨。

图:2002-2007年焦炭出口量及出口价格走势(美元/吨)

来源:国家统计局

预计2007-2008年国内粗钢表观消费量增长仍将保持在11%左右,这对国内焦炭需求将形成强有力的拉动因素,国内焦炭市场在钢材价格和炼焦成本的推动下也将对焦炭价格形成加固。

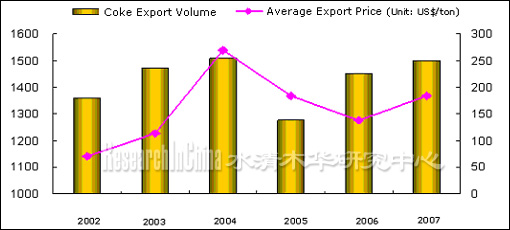

Coal-coking, as an auxiliary sector for the metallurgical industry, is the most mature sector in technology and the most representative of the coal chemical industry. China’s coking technology is advanced in the world and China is the biggest coke producer, consumer and exporter in the world. In recent years, coking market has had a gradual recovery, which has brought about a continuous rise in prices of coking products. We herein believe that the coking industry is on the upward trend from the perspective of industry cycles.

Since the second half of 2005, the average export price of coke had dropped dramatically. However, coke market had a rally in 2006 and once had the largest gain, hitting US$33 per ton, in the year. Since entering the year of 2007, the month-on-month growth in coke price has even picked up. The third quarter of 2007 had the biggest gain, which made coke price stand at US$203 per ton, representing an accumulated rise of nearly US$60/ton in coke price compared to US$144 per ton posted in the same period of 2006.

Export Volume and Export Price of China Coke, 2002-2007

Source: The National Bureau of Statistics of China

It is forested that in the period 2007 to 2008, China’s growth of apparent consumption volume of crude steel will remain around 11%, which will be a powerful impetus to coke demand in China. Domestic coke market, stimulated by steel price and coking cost, will also strengthen coke price.

第一章 煤化工行业概况

1.1煤化工产业链

1.2煤化工产业环境

1.2.1高油价:世界煤化工技术进步的动力

1.2.2资源约束:中国发展煤化工的必要性

1.2.3能源价格改革:增强煤化工替代优势

1.2.4传统煤化工处于成熟期

第二章 煤焦化政策环境

2.1煤焦化――加快行业结构调整

2.2上游煤炭行业政策

2.2.1控制煤炭产量

2.2.2改小建大,优化结构

2.2.3暂停探矿权

第三章 煤炭行业分析

3.1煤炭产业发展状况

3.1.1几年来煤炭消费量

3.1.2供煤炭产量增速将放缓

3.2煤价趋势分析---高煤价时代将会延续

3.2.1重化工业开始,能源消耗量大

3.2.2中长期我国煤炭资源紧缺性是高煤价的基础

3.2.3行业集中度的提高有利于政策性成本的转移

3.2.4高煤价时代将会继续

第四章 煤焦化市场分析

4.1焦炭市场分析

4.1.1炼焦煤涨价更具潜力

4.1.2焦炭市场需求

4.1.3焦炭市场供给

4.2煤焦油市场分析

4.2.1我国煤焦油需求结构与预测分析

4.2.2煤焦油出口形势分析

4.2.3煤焦化相关产品价格走势分析

4.2.4煤焦油加工业的未来发展方向

第五章 焦炭行业区域分析

5.1我国焦炭行业区域分布状况

5.2 2007-2008年初年山西省焦炭行业发展分析

5.2.1 2007年,山西焦炭市场需求较旺、价格回升

5.2.2 2008年以来山西省焦炭价格上涨

5.2.3.焦炭价格上涨原因分析

5.3河北省焦炭行业发展分析

5.3.1河北焦炭行业概况

5.3.2河北省焦炭市场发展状况

第六章 重点上市公司分析

6.1山西焦化

6.1.1公司简介

6.1.2公司发展方向

6.2安泰集团

6.2.1公司简介

6.2.2公司发展方向

6.3开滦股份

6.3.1公司简介

6.3.2公司主要业务状况

6.3.3焦炭分公司发展状况

6.3.4公司焦化下游产业链延伸

6.4太原煤气化股份有限公司---G煤气化

6.4.1公司简介

6.4.2公司主要业务状况

6.4.3公司焦炭业务发展方向

6.5黑化股份

6.5.1公司简介

6.5.2公司主营业务

6.6云维股份

6.6.1公司简介

6.6.2公司战略

6.7四川圣达

6.7.1公司介绍

6.7.2公司主要业务

6.7.3 公司战略

6.8国际实业

6.8.1公司简介

6.8.2公司主要业务

第七章 总结

1. General Situation of China Coal Chemical Industry

1.1. Industry Chain

1.2. Industry Environment

1.2.1. High Oil Price: Impetus to Advancement of World Coal Chemical Technology

1.2.2. Resources Restriction: Necessity of Developing Coal Chemical Industry in China

1.2.3 Energy Price Reform: Strengthening the Advantages of Coal Chemicals as Substitute

1.2.4 Traditional Coal Chemical Industry Is the Process of Becoming Maturity

2. Policy Environment for Coking Industry

1.1 Coking – Accelerating the Adjustments to Industry Structure

1.2 Policy of Upstream Coal Industry

2.2.1 To Control the Coal Output

2.2.2 To Build Big Companies by Merging Small Ones and Optimize the Industry Structure

2.2.3 To Suspend the Grant of Prospecting Right

3. Coal Industry

3.1 China Coal Industry Development

3.1.1 Coal Consumption in Recent Years

3.1.2 Growth in Coal Supply Will Slow Down

3.2 Coal Price Trend - High Price Will Extend

3.2.1 Heavy Chemical Industry Starts and Energy Consumption Increases

3.2.2 Coal Shortage Will Be the Base for High Coal Price

3.2.3 High Industry Concentration Degree Is Good to Transfer the Policy Cost

3.2.4 High Price Era Will Continue

4. Coking Market

4.1 Analysis of Coking Market

4.1.1 Coking Coal Has A Bigger Potential for Price Hikes

4.1.2 Demand of Coking Coal Market

4.1.3 Supply of Coking Coal Market

4.2 Coal Tar Market

4.2.1 Demand Structure and Forecast of China Coal Tar Market

4.2.2 Export of Coal Tar

4.2.3 Price Trend of Related Products

4.2.4 Development Trend of Coal Tar Industry in the Future

5. Analysis of Coking Industry by Region

5.1 Regional Distribution of China Coking Industry

5.2 Coking Industry Development in Shanxi province, 2007-2008

5.2.1 Strong Demand of Coking Market in Shanxi Province and Market Rally in 2007

5.2.2 Price Hikes in Shanxi Coking Market Since 2008

5.2.3 Factors Pushing Up Price

5.3 Coking Industry Development in Hebei Province

5.3.1 General Situation of Coke Market in Hebei Province

5.3.2 Coke Market Development in Hebei Province

6. Major Companies

6.1 Shanxi Coking Co., Ltd

6.1.1 Brief Introduction

6.1.2 Development Direction

6.2 Shanxi Antai Group Co., Ltd

6.2.1 Brief Introduction

6.2.2 Development Direction

6.3 Kailuan Clean Coal Co., Ltd

6.3.1 Brief Introduction

6.3.2 Major Businesses

6.3.3 Coking Subsidiary Company

6.3.4 Extension of Downstream Industry

6.4 Taiyuan Coal Gasification (Group) Co., Ltd

6.4.1 Brief Introduction

6.4.2 Major Businesses

6.4.3 Development Direction

6.5 Heilongjiang HeiHua Co., Ltd

6.5.1 Brief Introduction

6.5.2 Major Businesses

6.6 Yunnan Yunwei Co., Ltd

6.6.1 Brief Introduction

6.6.2 Company Strategy

6.7 Sichuan Shengda Industrial Co., Ltd

6.7.1 Brief Introduction

6.7.2 Major Businesses

6.7.3 Company Strategy

6.8 Xinjiang International Industry Co., Ltd

6.8.1 Brief Introduction

6.8.2 Major Businesses

7. Conclusion

图 1 煤化工产业链

图 2 1950-2005年国际原油价格变化趋势

图 3 中国化石能源储量结构

图 4 我国煤化工相关产品发展目标

图5 煤炭十一五规划2010 年产能

图 6 煤炭行业固定资产投资额与增速走势

图 7 煤炭行业固定资产投资占全社会固定资产投资比重

图 8 过去几年主要耗煤产业快速增长

图 9 2002-2010年煤炭产量变化趋势

图 10 2002-2010年煤炭产需比例变化趋势

图 11 “十一五”期间国内煤炭供求预测

图 12 重工业企业总产值占工业总产值比例

图 13 一次能耗总量(亿吨标煤,左轴)及其增速(右轴)

图 14 我国历年单位GDP 能耗(以2005 年不变价计)

图 15 一次能耗消费结构(%)

图 16 我国煤炭消费中长期预测表

图 17 世界煤炭储量分布

图 18 国有重点原煤产量占比明显上升

图 19 不同煤种占比情况

图 20 我国炼焦煤在各省份的分布情况

图 21 焦炭产量增速明显高于原煤产量增速

图 22 煤炭价格走势图(单位:元/吨)

图 23 06 年以来焦炭价格大幅度上涨

图 24 焦炭行业利润率提升

图 25 2004-2007年出口焦炭价格走势(美元/吨)

图 26 焦油深加工产品

图 27 焦炭企业销售毛利率比较(%)

图 28 焦炭企业净资产收益率比较(%)

图 29 安泰集团销售利润变动图

图 30 公司焦炭产销量大幅度增长

图 31 2007 年开滦地区焦煤煤坑口价涨幅

图 32 开滦地区焦炭价格走势图

图 33 焦炭价格、成本和毛利

图 34 焦炭毛利率

图 35 公司各项注音业务收入及同比增长

图 36 公司所在地煤炭和焦炭价格走势

图37 主营业务分行业,产品情况表

图38 主营业务收入向煤化工转变

图39 国际实业焦炭产量(万吨)

表 1 我国三类化石能源储、产量情况

表 2 中国三大能源热值价格与国际的比较:

表 3 不同煤种价格价格涨幅比较

表 4 2003年-2005年工业萘进出口数据

表 5 2002年-2007年煤焦油表观消费量 单位:万元/吨

表 6 山西焦化三个重点项目

表 7 山西焦化公司分业务盈利情况

表 8 焦炭子公司实现利润情况

表 9 煤炭和焦化业务实现净利润比较

表 10 开滦股份增发募集资金投资项目概况

表11 开滦股份主要产品产能统计

表12 云维股份与山西焦化产能对比

表13 国际实业未来几年内/外贸预测

表14 焦炭和煤焦油产量走势 单位:万吨

表15 2007年焦炭主要上市公司产量对比 单位:万吨

Selected Tables:

Reservation and Production of Three Fossils in China

Prices of Three Energies between China and International

Rising Prices of Different Coal Varieties

Import and Export of Crude Naphthalene 2003-2005

Apparent Consumption Volume of Coal Tar 2002-2007

Three Key Coking Projects in Shanxi

Profits of Shanxi Coking (Group) Co., Ltd, by Different Business

Profits of Coking Subsidiary Company

Comparison Profitability between Coal and Coking Businesses

Production Capacity of Kailuan Clean Co., Ltd’s Major Products

Investment Projects of Kailuan Clean Coal Co., Ltd

Production Capacity of Yunana Yunwei Group Co., Ltd and Shanxi Coking (Group) Co., Ltd

Domestic and Overseas Sales Xinjiang International Industry Co., Ltd in the Future Years

Production Trend of Coking Coal and Coal Tar

Output Comparison among Main Public Coking Companies in 2007

如果这份报告不能满足您的要求,我们还可以为您定制报告,请 留言说明您的详细需求。

|