|

|

|

报告导航:研究报告—

TMT产业—电信

|

|

2009年手机内存行业研究报告 |

|

字数:3.6万 |

页数:152 |

图表数:105 |

|

中文电子版:8000元 |

中文纸版:4000元 |

中文(电子+纸)版:8500元 |

|

英文电子版:2500美元 |

英文纸版:2300美元 |

英文(电子+纸)版:2800美元 |

|

编号:ZYW019

|

发布日期:2009-11 |

附件:无 |

|

|

|

NOR闪存在512Mb是个门槛。高于350Mb,NOR闪存的成本飞速增加。同时,NOR闪存的应用领域单一,应用厂家很少;而NAND闪存则容量越大,成本优势越明显,应用领域更广泛,应用厂家也多。手机市场变化迅速,现在每一款手机的生命周期通常都小于5年,NOR最强大的优势“长寿”也不复存在。尽管NOR闪存的成本在进入65纳米后也大幅度下降,但是专心NOR领域的只有Spansion。而NAND领域,三星、东芝、现代、美光、英特尔等实力大厂云集,NAND遇到的任何问题,都有大量的研究人员投入其中。曾经是手机内存第一名的Spansion黯然退出舞台。

高于350Mb,NAND取代了NOR闪存。对于手机NAND内存的容量,最初大部分厂家都认为没有必要太大,因为可以靠外接内存卡实现超大的容量。当少数厂家推出内置大容量NAND内存的机型明显更受市场欢迎,其他厂家也纷纷跟进。现在大部分手机内部NAND闪存容量越来越大,最大的有32Gb之多,而eMMC又推波助澜,使得智能手机最差也有1Gb的NAND容量。

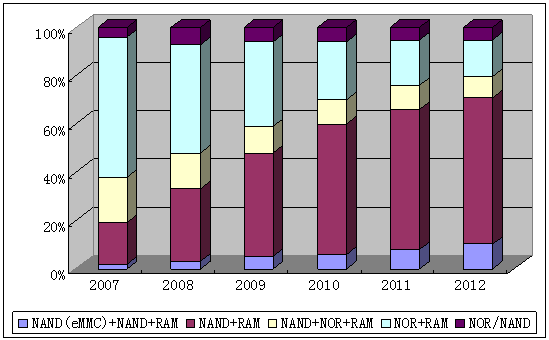

2007-2012年手机内存配置发展趋势

来源:水清木华研究中心

目前智能手机100%使用NAND+RAM型内存配置,大约60%的高端手机也采用NAND+RAM型内存配置。中低端手机一般采用NOR+RAM型内存配置,超低端手机大部分采用单NOR型内存配置。

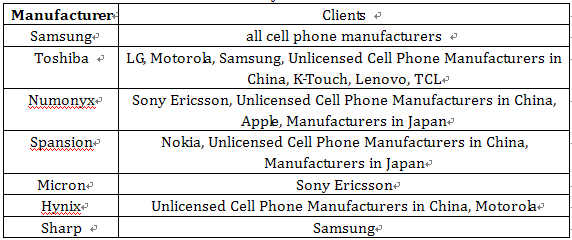

除苹果、索爱和诺基亚外,所有的智能手机厂家都采用三星的高容量内存。东芝在中端市场份额非常高。不过诺基亚对东芝的eMMC强力支持,其高端市场应该有比较大的发展空间。Numonyx主要客户有索爱、中国黑手机厂家、苹果、日本厂家,其缺乏RAM支持导致其NAND+RAM型内存发展缓慢。Spansion核心技术是NOR领域,在NAND和RAM领域都严重缺失。美光和现代则是后起之秀,两者都在NAND+RAM领域实力强大,有能力在将来抢占三星的市场份额。现代已经打入摩托罗拉供应商领域,未来LG也极有可能成为现代客户。

主要手机内存厂商及客户表

来源:水清木华研究中心

512Mb is a threshold in NOR flash memory, and the cost increases rapidly if it is higher than 350Mb. In addition, NOR flash memory has applied for limited fields and fewer clients. However, NAND flash memory has more and more cost advantages as capacity grows larger, and it has widely applied for more clients. Currently, the cell phone market changes rapidly, and the life cycle of a cell phone is usually less than five years, so NOR’s most outstanding advantage, long life, becomes meaningless as well. Although NOR flash memory cost will decline sharply after the entry of 65nm, Spansion is the sole which engages in NOR field. While in NAND, the powerful companies such as Samsung, Toshiba, Hynix, Micron and Intel all have gathered, and a large number of researchers will be involved once NAND has met any problems. Spansion, once No.1 in cell phone memory, has retreated from such field.

NAND will replace NOR flash memory if it is higher than 350Mb. The majority of manufacturers believed that it was not necessary that cell phones are with large-capacity NAND memory since they can rely on external memory card to achieve it. However, when cell phones with built-in large-capacity NAND memory launched by a small number of manufacturers have become popular, and others all have successively entered such field. Now, most of cell phone built-in NAND flash memory capacity becomes larger and larger, reaching 32 Gb at most, and promoted by eMMC, the smart phone NAND capacity is 1Gb at least.

Development Trend of Cell Phone Memory Configuration, 2007-2012

Source: ResearchInChina

Presently, all smart phones are provided with NAND+RAM memory, and around 60% of high-end cell phones have used NAND+RAM memory as well. In general, the medium and low-end cell phones adopt NOR+RAM memory, and most of ultra-low-end cell phones use NOR memory.

Except Apple, Sony Ericsson and Nokia, all smart phone manufacturers all adopt Samsung’s high-capacity memory. Toshiba has covered a high share in medium-end market, and Nokia’s support for eMMC has made Toshiba have larger development space. The main clients of Numonyx are Sony Ericsson, unlicensed cell phone manufacturers in China, Apple and manufacturers from Japan. Without support of RAM, Numonyx NAND+RAM memory has developed slowly. Spansion is adept in NOR, but serious lack of technologies for NAND and RAM. Being the new comers, Micron and Hynix both have shown powerful strength in NAND+RAM field, and they are capable of seizing market share from Samsung. Hynix has become Motorola’s supplier, and LG is also with great possibility to become another customer.

Main Cell Phone Memory Manufacturers and Clients

Source: ResearchInChina

第一章:内存行业现状与未来

1.1、手机嵌入式内存简介

1.2、手机内存发展

1.3、手机内存市场与产业

1.4、手机内存封装

1.5、DRAM产业现状

1.6、DRAM封装

1.7、NAND闪存产业现状

1.8、NAND闪存未来发展趋势

1.9、NAND闪存封装发展

1.10、SSD

1.11、NAND 控制IC产业

1.12、EMMC

1.13、BA NAND 、EMMC、LBA NAND格式战

第二章:手机市场与产业

1.1、全球手机市场

2.2、全球手机产业

2.3、中国手机市场

2.4、中国手机出口

2.5、中国手机产业

第三章:手机厂家内存研究

3.1、诺基亚

3.2、摩托罗拉

3.3、三星

3.4、索尼爱立信

3.5、LG

3.6、RIM

3.7、苹果

3.8、宏达国际电子

3.9、中国手机内存研究

第四章:内存厂家研究

4.1、三星

4.2、旺宏

4.3、华亚科技

4.4、力晶

4.5、HYNIX

4.6、ELPIDA

4.7、NUMONYX

4.8、东芝

4.9、SPANSION

4.10、MICRON

4.11、华邦

4.12、SST

4.13、钰创

4.14、晶豪科技

1 Status Quo and Future of Cell Phone Memory

1.1 Built-in Memory

1.2 Development

1.3 Market & Industry

1.4 Packaging

1.5 DRAM Industry

1.6 DRAM Packaging

1.7 NAND Flash Memory Industry

1.8 NAND Flash Memory Development

1.9 NAND Flash Memory Packaging Development

1.10 SSD

1.11 NAND Control-IC Industry

1.12 EMMC

1.13 BA NAND, EMMC and LBA NAND

2 Cell Phone Market & Industry

1.1 Global Cell Phone Market

2.2 Global Cell Phone Industry

2.3 China’s Cell Phone Market

2.4 China’s Cell Phone Export

2.5 China’s Cell Phone Industry

3 Memory of Cell Phone Manufacturers

3.1 Nokia

3.2 Motorola

3.3 Samsung

3.4 Sony Ericsson

3.5 LG

3.6 RIM

3.7 Apple

3.8 HTC

3.9 Study on China’s Cell Phone Memory

4 Memory Manufacturers

4.1 Samsung

4.2 Macronix

4.3 Inotera

4.4 PowerChip

4.5 HYNIX

4.6 ELPIDA

4.7 NUMONYX

4.8 Toshiba

4.9 SPANSION

4.10 MICRON

4.11 Winbond

4.12 SST

4.13 Etron

4.14 ESMT

手机嵌入式内存发展路线图

2007-2012年手机内存配置发展趋势

2007-2012年NAND+RAM型手机内存容量变化趋势

2007-2012年NOR+RAM型手机内存容量变化趋势

2007-2012年手机内存市场规模统计及预测

2009年手机内存主要厂家市场占有率

2007-2010年手机单芯片内存封装趋势

2007-2011年SIP手机内存封装发展趋势

2007-2011年PoP手机内存发展趋势

2008-2012年SSD下游应用分布

2007-2009年2季度全球手机出货量地域分布

2009年上半年中国大陆主要手机厂家市场占有率

1999-2008年中国手机出口量统计及预测

2002-2008年中国手机出口金额统计及预测

2008年1-12月每月出货量与平均价格统计

2007年1季度到2009年3季度诺基亚手机地域出货量结构统计

2007年1季度到2009年3季度诺基亚手机出货量与平均销售价格统计

2007年1季度到2009年3季度诺基亚手机出货量与运营利润率统计

诺基亚2006年1季度到2009年3季度每季度手机中国地区出货量统计

2009年诺基亚内存供应商供应比例

2009年摩托罗拉手机内存供应商供应比例

三星2001-2008年手机出货量与年增幅统计

三星2006年1季度到2009年3季度每季度手机出货量统计

2006年1季度到2009年3季度三星手机出口平均价格与运营利润率统计

三星2009年手机内存供应商供应比例

2006年1季度到2009年3季度索尼爱立信出货量与平均销售价格统计

2006年1季度到2009年3季度索尼爱立信收入与运营利润率统计

2001-2008年LG手机出货量与年增幅统计

2007年1季度到2009年3季度LG手机每季度出货量(按制式)

2007年1季度到2009年3季度LG手机每季度销售额与运营利润统计

2007年1季度到2009年3季度LG 手机部门地域收入结构

LG 2007年1季度到2009年3季度销售额、平均价格统计

2009年LG手机内存供应商供应比例

2006-2008年宏达电地域收入结构比例

2008年1季度-2009年2季度宏达电出货量与平均价格统计

2008年1季度-2009年2季度宏达电收入与年度增长率统计

2009年中国手机内存主要厂家市场占有率

三星的手机内存发展路线图

2003-2010年旺宏收入与毛利率统计及预测

2007年1季度-2009年2季度旺宏每季度毛利率统计

2008年2季度、2009年1、2季度旺宏收入部门分布

2008年2季度、2009年1、2季度旺宏出货量部门分布

2008年2季度、2009年1、2季度旺宏收入技术分布

2008年2季度、2009年1、2季度旺宏收入地域分布

2004年1季度-2009年2季度旺宏折合8英寸晶圆出货量与平均产能利用率

2004年1季度-2009年2季度旺宏ROM出货量

2004年1季度-2009年2季度旺宏FLASH出货量

2008年1季度-2009年2季度旺宏FLASH收入技术分布

2009年2季度旺宏NOR FLASH下游应用分布

2004-2010年华亚科技收入与毛利率统计及预测

华亚科技2008年1季度-2009年3季度收入与毛利率统计

2003-2009年华亚科技资本支出额度及用途

2008年1季度-2009年3季度HYNIX收入产品分布

2008年1季度-2009年3季度HYNIX收入与毛利率统计

2009年1季度-2010年4季度HYNIX收入产品分布

2005-2010年HYNIX 收入与毛利统计及预测

HYNIX手机用MCP内存型号解码

2005-2009财年ELPIDA收入部门分布

ELPIDA 2006年-2009年工厂制程分布

ELPIDA路线图

2005财年-2011财年东芝收入与运营利润统计及预测

2007-2012财年东芝收入部门分布

2008-2010财年1季度东芝半导体收入产品分布

东芝2005-2009年产品收入结构比例

东芝半导体2003-2009财年各领域投资统计及预测

2004-2009年Spansion收入与毛利率统计及预测

2007年1季度-2008年3季度Spansion收入部门分布

2007年1季度-2008年3季度Spansion的EBITDA与毛利率统计

2007-2008年3季度Spansion费用所占比例

Spansion全球分布

2006-2008年Spansion生产工艺技术结构

FAB25 厂生产工艺路线图

SP1厂生产工艺路线图

Spansion成本估算演进图

2004-2009财年美光科技收入与毛利统计

2007年1季度-2009年3季度美光科技收入与毛利率统计

2005-2009财年前9月美光收入产品分布

21006-2010年华邦收入与毛利率统计及预测

2008年1季度-2009年3季度华邦收入与毛利率统计

2008年1季度-2009年1季度华邦内存制程分布

2009年2、3季度华邦收入产品分布

2003-2009年前9月SST收入与毛利率统计

2005-2009年前9月SST收入地域分布

2008年1季度-2009年3季度SST收入下游应用分布

2001-2010年钰创收入与毛利率统计及预测

2001-2009年晶豪科技收入与毛利率统计及预测

NAND控制IC厂商一览

2007-2009年上半年全球品牌手机出货量排名

2008上半年、2009上半年中国14大手机厂家产量排名

2008上半年、2009上半年中国32大手机厂家出口量排名

2007、2008、2009年上半年南北诺基亚出口量统计

2007、2008、2009年上半年南北诺基亚产量统计

诺基亚50款典型手机内存配置

2007、2008、2009年上半年摩托罗拉中国出口量产量统计

摩托罗拉15款手机内存配置

2007、2008、2009年天津三星、惠州三星、三星科健出口量、产量统计

31款三星典型手机内存配置

2006、2007、2008、2009年上半年索尼爱立信中国出口量与产量

索爱手机平台一览

2007、2008、2009年LG烟台与青岛出口量 统计

LG 13款典型手机零组件配置清单

HTC 11款手机内存配置

50款中国手机内存配置

旺宏各部门简介

英特尔闪存特性

意法半导体手机领域用内存产品一览

东芝手机用MCP产品

Cell Phone Built-in Memory Development

Development Trend of Cell Phone Memory Configuration, 2007-2012E

NAND+RAM Cell Phone Memory Capacity, 2007-2012E

NOR+RAM Cell Phone Memory Capacity, 2007-2012E

Cell Phone Memory Market Size, 2007-2012E

Market Shares of Key Cell Phone Memory Manufacturers, 2009

Cell Phone Single-chip Memory Packaging Trend, 2007-2010

SIP Cell Phone Memory Packaging Trend, 2007-2011

PoP Cell Phone Memory Packaging Trend, 2007-2011

SSD Distribution by Downstream Application, 2008-2012

Global Cell Phone Shipment by Region, 2007-2009Q2

Market Shares of Key Mainland China Cell Phone Manufacturers, 1H2009

China Cell Phone Export Volume, 1999-2008

China Cell Phone Export Value, 2002-2008

Monthly Shipment and Average Price, Jan-Dec, 2008

Nokia Cell Phone Shipment by Region, 2007Q1-2009Q3

Nokia Cell Phone Shipment and Average Selling Price, 2007Q1-2009Q3

Nokia Cell Phone Shipment and Operating Profit Margin, 2007Q1-2009Q3

Nokia Quarterly Cell Phone Shipment in China, 2006Q1-2009Q3

Supply Ratio of Nokia Memory Suppliers, 2009

Supply Ratio of Motorola Cell Phone Memory Suppliers, 2009

Samsung Cell Phone Shipment and Growth Margin, 2001-2008

Samsung Quarterly Cell Phone Shipment, 2006Q1-2009Q3

Samsung Cell Phone Average Export Price and Operating Profit Margin, 2006Q1-2009Q3

Supply Ratio of Samsung Cell Phone Memory Suppliers, 2009

Sony Ericsson Shipment and Average Selling Price, 2006Q1-2009Q3

Sony Ericsson Revenue and Operating Profit Margin, 2006Q1-2009Q3

LG Cell Phone Shipment and Annual Growth Margin, 2001-2008

LG Quarterly Cell Phone Shipment by Network Format, 2007Q1-2009Q3

LG Quarterly Cell Phone Sales and Operating Profit, 2007Q1-2009Q3

LG Cell Phone Revenue by Region, 2007Q1-2009Q3

LG Sales and Average Price, 2007Q1-2009Q3

Supply Ratio of LG Cell Phone Memory Suppliers, 2009

HTC Revenue by Region, 2006-2008

HTC Shipment and Average Selling Price, 2008Q1-2009Q2

HTC Revenue and Annual Growth Rate, 2008Q1-2009Q2

Market Shares of Main China’s Cell Phone Memory Manufacturers, 2009

Samsung’s Cell Phone Memory Development Roadmap

Macronix Revenue and Gross Profit Margin, 2003-2010E

Macronix Quarterly Gross Profit Margin, 2007Q1-2009Q2

Macronix Revenue by Division, 2008Q2-2009Q1&Q2

Macronix Shipment by Division, 2008Q2-2009Q1&Q2

Macronix Revenue by Technology, 2008Q2-2009Q1&Q2

Macronix Revenue by Region, 2008Q2-2009Q1&Q2

Macronix 8-inch Wafer Shipment and Average Capacity Utilization Ratio, 2004Q1-2009Q2

Macronix ROM Shipment, 2004Q1-2009Q2

Macronix FLASH Shipment, 2004Q1-2009Q2

Macronix FLASH Revenue by Technology, 2008Q1-2009Q2

Macronix NOR FLASH Distribution by Downstream Application, 2009Q2

Inotera Revenue and Gross Profit Margin, 2004-2010

Inotera Revenue and Gross Profit Margin, 2008Q1-2009Q3

Inotera Capital Expenditure and Usage, 2003-2009

HYNIX Revenue by Product, 2008Q1-2009Q3

HYNIX Revenue and Gross Profit Margin, 2008Q1-2009Q3

HYNIX Revenue by Product, 2009Q1-2010Q4

HYNIX Revenue and Gross Profit Margin, 2005-2010

HYNIX’s Cell Phone MCP Decoding by Type

ELPIDA Revenue by Division, FY2005 - FY2009

ELPIDA Plants by Process, 2006-2009

ELPIDA Roadmap

Toshiba Revenue and Operating Profit, FY2005-FY2011

Toshiba Revenue by Division, FY2007-FY2012

Toshiba Semiconductor Revenue by Product, FY2008 -FY2010

Toshiba Revenue by Product, 2005-2009

Toshiba Semiconductor Investment by Field, FY2003-FY2009

Spansion Revenue and Gross Profit Margin, 2004-2009

Spansion Revenue by Division, 2007Q1-2008Q3

Spansion EBITDA and Gross Profit Margin, 2007Q1-2008Q3

Spansion Expenditure Ratio, 2007-2008Q3

Spansion Global Presence

Spansion Production Technology Structure, 2006-2008

FAB25 Plant Production Technology Roadmap

SP1 Plant Production Technology Roadmap

Spansion Cost Estimation

MICRON Revenue and Gross Profit, FY2004-FY2009

MICRON Revenue and Gross Profit Margin, 2007Q1-2009Q3

MICRON Revenue by Product, 2005FY-Sep, FY2009

Winbond Revenue and Gross Profit Margin, 2006-2010

Winbond Revenue and Gross Profit Margin, 2008Q1-2009Q3

Winbond Memory by Process, 2008Q1-2009Q1

Winbond Revenue by Product, Q2-Q3, 2009

SST Revenue and Gross Profit Margin, 2003-Sep, 2009

SST Revenue by Region, 2005-Sep, 2009

SST Revenue by Downstream Application, 2008Q1-2009Q3

Etron Revenue and Gross Profit Margin, 2001-2010

ESMT Revenue and Gross Profit Margin, 2001-2009

NAND Control IC Manufacturers

Ranking of Global Cell Phone Brands by Shipment, 2007-1H2009

Top 14 China’s Cell Phone Manufacturers by Output, 1H2008-1H2009

Top 32 China’s Cell Phone Manufacturers by Export Volume, 1H2008-1H2009

Nokia South and North Export Volume, 2007, 2008 & 1H2009

Nokia South and North Output, 2007, 2008 & 1H2009

Memory Configuration of Nokia’s 50 Models

Motorola Export Volume and Output in China, 2007, 2008 & 1H2009

Memory Configuration of Motorola’s 15 Models

Export Volume and Output of Tianjin Samsung, Huizhou Samsung and Samsung Kejian, 2007, 2008 & 1H2009

Memory Configuration of Samsung’s 31 Models

Song Ericsson Export Volume and Output in China, 2007, 2008 & 1H2009

Song Ericsson Cell Phone Platform

Export Volumes of LG Yantai and Qingdao, 2007, 2008 & 2009

Parts Configuration of LG’s 13 Models

Memory Configuration of HTC’s 11 Models

Memory Configuration of China’s 50 Cell Phone Models

Profile of Macronix’s Departments

Intel Flash Memory Property

STM’s Memory Products for Cell Phone

Toshiba’s MCP Products for Cell Phone

如果这份报告不能满足您的要求,我们还可以为您定制报告,请 留言说明您的详细需求。

|