|

|

|

报告导航:研究报告—

TMT产业—电子半导体

|

|

2012-2013年全球及中国先进封装行业研究报告 |

|

字数:2.7万 |

页数:162 |

图表数:185 |

|

中文电子版:8500元 |

中文纸版:4250元 |

中文(电子+纸)版:9000元 |

|

英文电子版:2500美元 |

英文纸版:2600美元 |

英文(电子+纸)版:2800美元 |

|

编号:ZYW149

|

发布日期:2013-05 |

附件:下载 |

|

|

|

<2012-2013年全球及中国先进封装行业研究报告>包括以下内容:1、全球半导体产业概况

2、IC制造产业概况

3、IC下游行业市场概况

4、先进封装产业与市场

5、23家先进封装厂家研究

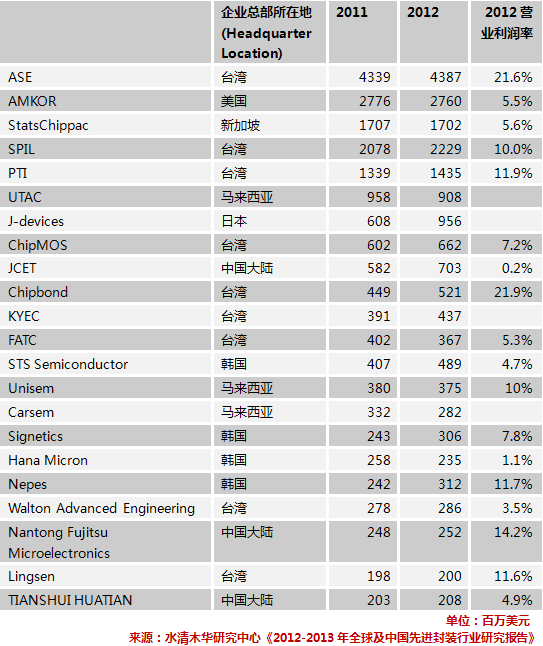

2012年全球半导体销售额下滑了2.7%;半导体设备开支下滑了15%,从2011年的435亿美元下滑到了369亿美元。2013年的半导体市场也不容乐观,全球新兴经济体全面衰退,欧洲复苏乏力。美国和日本市场相对好一些,但作为全球最大半导体市场的中国,经济增速低于预期,全球经济仍然未出现复苏的迹象。 虽然半导体产业整体下滑,但在晶圆代工(Foundry)领域仍然呈现增长, 2012年全球半导体晶圆代工市场总值达346亿美元,较2011年成长6.5%。随着智能手机、平板电脑增速放缓,预计2013年晶圆代工市场仅增长1.6%,约352亿美元以上。 先进封装厂家主要客户就是晶圆代工厂家,因此2012年先进封装厂家基本持平或微幅增长,预计2013年也是如此。黄金是先进封装厂家尤其是LCD Driver IC封装厂家必须使用的原材料,2013年金价下跌,将提高先进封装厂家的利润率。 位于马来西亚和新加坡的厂家都出现了下滑,因为这一地区的晶圆代工厂收入下滑。台湾厂家除内存封装外都有小幅度增长,主要是受益于TSMC、UMC的强力拉动。韩国企业则受益于三星的拉动。 日本企业J-devices增幅最大,主要是富士通将后端封装业务出售给了J-devices。2013年1月,日本最大的半导体厂家Renesas也将3座后端封装业务工厂出售给J-devices,2013年J-devices将会有惊人的增长,该公司预计2013财年收入超过1000亿日元,2017财年收入超过2500亿日元。 2013年表现会很好的还有台湾的Chipbond,该公司是全球最大的LCD Driver IC封装厂家。目前手机、平板电脑的屏幕分辨率(Resolution)都大幅度提升,这会大幅提高Chipbond的收入规模。黄金是Chipbond主要的原材料,金价下跌,Chipbond是最大受益者。为进一步完善产业链布局,2013年5月2日,Chinbond收购了COF Substrate厂家SIMPAL ELECTRONICS 。 Chipbond还是营业利润率最高的先进封装厂家,其营业利润率在2011年是16.7%,2012年达到21.9%。也是唯一一家营业利润率增长的公司。ASE的营业利润率紧随Chipbond,主要因为其大客户TSMC制造的都是全球最顶尖的IC,ASE也因此具备较高的利润率。 中国大陆厂家表现不佳,JECT虽然收入大幅度增长,但是营业利润率大幅下跌,从2011年的1.8%跌至2012年的0.2%,处于亏损边缘。 2011-2012年全球前23大封测厂家收入与营业利润率

Global and China Advanced Packaging Industry Report, 2012-2013 covers the followings: 1. Global Semiconductor Industry Overview; 2. IC Manufacturing Industry Overview; 3. IC Downstream Industry Market Overview; 4. Advanced Packaging Industry and Market; 5. 23 Advanced Packaging Vendors In

2012, global semiconductor sales fell 2.7%; semiconductor equipment

spending dropped by 15% to US$36.9 billion from US$43.5 billion in 2011.

The semiconductor market in 2013 is also not optimistic, accompanied by

recession of the world’s emerging economies and Europe’s sluggish

recovery. U.S. and Japanese markets are relatively better, while China,

as the world’s largest semiconductor market, has witnessed

lower-than-expected economic growth, the global economy is yet to show

signs of recovery. In spite of the overall decline in

semiconductor industry, the foundry field still grows. In 2012, the

global semiconductor foundry market reached total value of US$34.6

billion, an increase of 6.5% over 2011. With the growth slowdown of

smart phones and tablet PCs, it is expected that the foundry market in

2013 will increase by just 1.6% to exceed about US$35.2 billion. With

foundries as main customers, advanced packaging vendors were therefore

essentially flat or slightly enhanced in 2012, the same expected in

2013. The fall in price of gold, the indispensable raw material for

advanced packaging vendors, especially LCD Driver IC packaging

companies, will improve the profit margin of advanced packaging vendors

in 2013. Vendors located in Malaysia and Singapore all showed

decline, on account of the decreasing revenue of foundries in this

region. Taiwanese peers saw moderate growth except memory package,

chiefly benefiting from the strong drive of TSMC and UMC. South Korean

companies were boosted by Samsung. Among Japanese companies,

J-devices experienced the highest growth, mainly owing to the back-end

packaging business purchased from Fujitsu. In January, 2013, Japan’s

largest semiconductor vendor – Renesas also sold three back-end

packaging factories to J-devices, which would usher in amazing growth in

the coming year, with expected annual revenue in FY2013 and FY2017

outnumbering JPY100 billion and JPY250 billion, respectively. Taiwan-based

Chipbond, the world’s largest LCD Driver IC packaging vendor, will be

another eye-catching performer in 2013. The significantly enhanced

screen resolution of mobile phone and tablet PC will greatly raise

Chipbond’s earnings, and the decline in gold prices makes it the biggest

beneficiary. In order to further improve the industrial chain layout,

Chipbond acquired the COF substrate vendor - SIMPAL Electronics on May

2, 2013. In addition, Chipbond is the advanced packaging vendor

with the highest operating margin, i.e. 16.7% in 2011 and 21.9% in 2012,

but also the unique one with operating margin growth. ASE closely

followed in terms of operating margin, who benefitted from its large

customer TSMC that produced the world’s state-of-the-art IC. Chinese

Mainland counterparts performed poorly, although JECT’s revenue saw

substantial growth, yet its operating margin fell sharply from 1.8% in

2011 to 0.2% in 2012, slipping to the edge of loss. Revenue and Operating Margin of the World’s Top 23 Packaging & Testing Vendors, 2011-2012

第一章、全球半导体产业

1.1、全球半导体产业概况

1.2、中国IC市场

第二章、半导体产业格局

2.1、模拟半导体

2.2、MCU

2.3、DRAM内存产业

2.3.1、DRAM内存产业现状

2.3.2、DRAM内存厂家市场占有率

2.3.3、移动DRAM内存厂家市场占有率

2.4、NAND闪存

2.5、复合半导体产业

第三章、IC制造产业

3.1、 IC制造产业概况

3.2、晶圆代工

3.3、MEMS代工

3.4、中国晶圆代工产业

3.5、晶圆代工市场

3.5.1、全球手机市场规模

3.5.2、手机品牌市场占有率

3.5.3、智能手机市场与产业

3.5.4、PC市场

3.6、IC制造与封测设备市场

3.7、半导体材料市场

第四章、封测市场与产业

4.1、封测市场规模

4.2、封测产业格局

4.3、WLCSP市场

4.4、TSV封装

4.5、FLIP-CHIP

4.6、半导体测试

4.7、全球封测厂家排名

第五章、封测厂家研究

5.1、日月光

5.2、安靠Amkor

5.3、矽品精密SPIL

5.4、星科金朋

5.5、力成PTI

5.6、超丰Greatek

5.7、南茂科技ChipMOS

5.8、京元电子KYEC

5.9、Unisem

5.10、福懋科技FATC

5.11、江苏长电科技JECT

5.12、UTAC

5.13、菱生精密

5.14、南通富士通微电子

5.15、华东科技

5.16、颀邦科技Chipbond

5.17、J-DEVICES

5.18、MPI

5.19、STS Semiconductor

5.20、Signetics

5.21、Hana Micron

5.22、Nepes

5.23、天水华天科技

1. Global Semiconductor Industry

1.1 Overview

1.2 China IC Market

2. Semiconductor Industry Pattern

2.1 Analog Semiconductor

2.2 MCU

2.3 DRAM Industry

2.3.1 Status Quo

2.3.2 Market Share of DRAM Vendors

2.3.3 Market Share of Mobile DRAM Vendors

2.4 NAND Flash

2.5 Compound Semiconductor Industry

3. IC Manufacturing

3.1 Overview

3.2 Foundry

3.3 MEMS Foundry

3.4 China Foundry Industry

3.5 Foundry Market

3.5.1 Global Mobile Phone Market Size

3.5.2 Market Share of Mobile Phone Brands

3.5.3 Smartphone Market and Industry

3.5.4 PC Market

3.6 IC Manufacturing and Packaging & Testing Equipment Market

3.7 Semiconductor Materials Market

4. Packaging & Testing Market and Industry

4.1 Market Size

4.2 Industry Pattern

4.3 WLCSP Market

4.4 TSV Packaging

4.5 FLIP-CHIP

4.6 Semiconductor Testing

4.7 Global Vendor Ranking

5. Packaging & Testing Vendors

5.1 ASE

5.2 Amkor

5.3 SPIL

5.4 STATS ChipPAC

5.5 PTI

5.6 Greatek

5.7 ChipMOS

5.8 KYEC

5.9 Unisem

5.10 FATC

5.11 JECT

5.12 UTAC

5.13 Lingsen Precision

5.14 Nantong Fujitsu Microelectronics

5.15 Walton Advanced Engineering

5.16 Chipbond

5.17 J-DEVICES

5.18 MPI

5.19 STS Semiconductor

5.20 Signetics

5.21 Hana Micron

5.22 Nepes

5.23 Tian Shui Hua Tian Technology

1989-2016年全球IC市场规模

1990年4季度-2013年2季度全球半导体ASP

2011年1月-2013年3月半导体Book-to-Bill Ratio

1994-2012年全球晶圆产能变化

2011年全球前25大半导体厂家销售额排名

2012年全球前25大半导体厂家销售额排名

2011年模拟半导体主要厂家市场占有率

2011年Catalog 模拟半导体厂家市场占有率

2011年10大模拟半导体厂家排名

2011年MCU厂家排名

2008-2016年全球DRAM与NAND市场规模

2000-2013年DRAM产业CAPEX

2000-2013年全球DRAM出货量

2012年7月-2013年3月DRAM合约价涨跌幅

2010年1季度-2014年4季度DRAM Supply And Demand

2010年1季度-2014年4季度PC DRAM Supply And Demand

2009-2014年DRAM下游市场分布

2001-2013年 系统内存需求量

2011年4季度DRAM品牌厂商收入排名

2012年4季度品牌Dram厂商收入排名

2009-2011年Mobile DRAM 市场份额

2012年Mobile DRAM 市场份额

2012 年 品牌NAND Flash厂家市场份额

2009-2014年NAND下游市场分布

GaAs产业链

GaAs产业链主要厂家

2011-2012年全球GaAs厂家收入排名

2012年12月全球各地区Fab Installed Capacity by Minimum Geometry

2012年12月全球各地区Fab Installed Capacity by Product Type

2011年全球12英寸晶圆产能

2013全球12英寸晶圆产能

1999-2012年全球12英寸晶圆厂产能地域分布

2011年4季度-2012年4季度主要Fab支出产品分布

2010年1季度-2013年4季度全球晶圆加载产能产品分布

2010-2012年全球晶圆设备开支地域分布

2005-2012年全球Foundry销售额排名

2005-2012年全球主要Foundry运营利润率

2011年全球前30家MEMS厂家收入排名

2012年全球前20大MEMS Foundry排名

2011年中国Foundry销售额

2011年全球前25家IC设计公司排名

2008-2016年平均每部手机IC成本

2007-2014年全球手机出货量

2010-2013年全球CDMA/WCDMA手机出货量地域分布

2010-2011年每季度全球主要手机品牌出货量

2011-2012年全球主要手机厂家出货量

2012年4季度全球智能手机操作系统分布

2011-2012中国主要智能手机厂家出货量

2008-2013年全球PC用CPU与GPU 出货量

2012、2013年平板电脑主要厂家产量

2012-2014年 SE ASIA Fab分产品类型设备支出

2011-2014 SE Asia分产品产能

2007-2016全球晶圆设备投入规模

2011-2016年全球WLP封装设备开支

2011-2016年全球Die封装设备开支

2011-2016年全球自动检测设备开支

2011-2012年全球TOP 10 半导体厂家资本支出额

2013年全球TOP 10 半导体厂家CAPEX

2010-2013年全球半导体材料市场地域分布

2010-2012年全球半导体后段设备支出地域分布

2006-2014年OSAT市场规模

2007年全球IC封装类型出货量分布

2010年全球IC封装类型出货量分布

2012年全球IC封装类型出货量分布

2016年全球IC封装类型出货量分布

2007、2011、2015年全球封测市场技术分布

2012年全球OSAT产值地域分布

2014年全球OSAT产值地域分布

2007-2011年台湾封测产业收入

2010-2016年WLCSP封装市场规模

2010-2016年WLCSP出货量下游应用分布

手机CPU与GPU封装路线图

2012年FC封装下游市场分布

2002-2019年FC-BGA 技术趋势

2008-2012年全球前24大封测厂家收入与营业利润率

日月光组织结构

2005-2013年日月光收入与毛利率

2010-2012年日月光收入业务分布

2010年1季度-2011年4季度日月光铜线邦定收入

2010年1季度-2011年4季度日月光铜线邦定转换率

2010年1季度-2011年4季度日月光铜线邦定收入地理分布

2010年1季度-2011年4季度日月光铜线邦定 收入客户分布

2010年1季度-2013年1季度日月光封装部门收入、毛利率

2011年1季度-2013年1季度日月光封装部门收入类型分布

2010年1季度-2013年1季度日月光测试部门收入、毛利率

2010年1季度-2012年1季度日月光测试部门收入业务分布

2010年1季度-2013年1季度日月光材料部门收入、毛利率、运营利润率

2010年1季度-2013年1季度日月光 CAPEX与EBITDA

2012年1季度日月光10大客户

2013年1季度日月光收入下游应用

日月光中国分布

日月光上海封装类型

2004-2011年日月光上海收入

2005-2011年安靠收入与毛利率、运营利润率

2007-2012年安靠收入封装类型分布

2008年4季度-2012年4季度安靠收入封装类型分布

2008年4季度-2012年4季度安靠出货量封装类型分布

2011年安靠 CSP封装收入下游应用分布

2011年安靠 BGA封装收入下游应用分布

2011年3季度安靠 Leadframe封装收入下游应用分布

2011年3季度安靠收入与出货量地域分布

2012年安靠收入与出货量地域分布

2008年1季度-2013年1季度安靠封装业务产能利用率

2011年1季度-2013年1季度Amkor收入下游市场分布

2011-2012年安靠成本结构

矽品精密工业组织结构

2003-2013年矽品收入、毛利率、运营利润率

2011年3月-2013年3月矽品月度收入与增幅

2005-2012年4季度矽品收入地域分布

2005-2012年4季度矽品收入下游应用分布

2005-2012年4季度矽品收入业务分布

矽品2006年1季度、2007年2、3季度、2011年3、4季度产能统计

2011年3季度-2012年4季度Copper/Ag Alloy 季度收入

2004-2013年星科金朋收入与毛利率

2006-2012年1季度星科金朋收入封装类型分布

2006-2013年1季度星科金朋收入下游应用分布

2006-2013年星科金朋收入 地域分布

2006-2013年力成科技收入与运营利润率

2011年3月-2013年3月力成科技月度收入与增幅

力成科技工厂一览

力成科技的TSV解决方案

2012年4季度力成科技收入业务分布

2012年4季度力成科技收入产品分布

2005-2013年超丰电子收入、毛利率、运营利润率

2007-2010年超丰电子收入技术类型分布

2011年3月-2013年3月超丰电子月度收入与增幅

2003-2013年南茂科技收入与毛利率

2010-2012年南茂科技收入业务分布

2010-2012年南茂科技收入产品分布

2009-2012年南茂科技Utilization Rate 和EBITDA Margin

2009-2012年南茂科技Cash Flow 和CAPEX

2011年南茂科技收入客户分布

2006-2011年南茂科技收入地域分布

2002-2013年京元电子收入与毛利率

2011年3月-2013年3月京元电子月度收入

京元电子厂房分布

京元电子TESTING PLATFORMS

2006-2013年Unisem收入与EBITDA

2010年1季度-2012年4季度 Unisem收入与EBITDA

2012年Unisem收入产品分布

2012年Unisem收入市场分布

台塑集团组织结构

福懋科技组织结构

2006-2013年福懋科技收入与运营利润率

2011年3月-2012年3月福懋科技月度收入

2006-2013年JECT收入与运营利润率

2011-2012年JECT产量、销量

2011-2012年JECT 测试成本结构

2011-2012年JECT 封装成本结构

JCET路线图

2011年JCET收入地域分布

2007-2013年菱生精密收入与运营利润率

2011年3月-2013年3月菱生精密月度收入

2006-2011年南通富士通微收入与增幅

2006-2011年南通富士通微净利润与增幅

2006-2011年南通富士通微季度收入与增幅

2006-2011年南通富士通微季度净利润与增幅

2006-2011年南通富士通微季度毛利率

2006-2011年南通富士通微季度A、S、R&D

2007-2013年华东科技收入与运营利润率

2011年3月-2013年3月华东科技月度收入与增幅

2006-2013年颀邦科技收入与运营利润率

2011年3月-2013年3月颀邦科技月度收入与增幅

2012年颀邦科技收入业务分布

2009年4季度-2012年1季度欣邦收入产品分布

2012年颀邦科技收入市场分布

J-Devices 组织结构

2007-2013财年MPI收入与税前利润

MPI收入地域分布

Carsem 2011年1季度-2012年1季度收入产品分布

STS Semiconductor组织结构

2006-2013年STS Semiconductor收入与运营利润率

2012年1季度-2013年4季度STS Semiconductor收入产品分布

Signetics股东结构

2007-2013年Signetics收入与运营利润率

2010年1季度-2012年4季度 Signetics产能利用率(Utilization)与运营利润率

2011年Signetics收入产品分布

2011年Signetics收入客户分布

2012年1季度-2013年4季度 Signetics收入技术分布

2006-2013年Hana Micron收入与运营利润率

2011年Hana Micron收入客户分布

2012年1季度-2013年4季度Hana Micron收入市场分布

2007-2013年Nepes收入与运营利润率

2012-2013年Nepes季度收入与运营利润率

2012-2013年Nepes季度收入部门分布

2006-2013年天水华天收入与运营利润率

Global IC Market Size, 1989-2016

Global Semiconductor ASP, Q4 1990-Q2 2013

Semiconductor Book-to-Bill Ratio, Jan. 2011-Mar. 2013

Global Wafer Capacity Change, 1994-2012

Ranking of the World’s Top 25 Semiconductor Vendors by Sales, 2011

Ranking of the World’s Top 25 Semiconductor Vendors by Sales, 2012

Market Share of Leading Analog Semiconductor Vendors, 2011

Market Share of Catalog Analog Semiconductor Vendors, 2011

Ranking of Top 10 Analog Semiconductor Vendors, 2011

Ranking of MCU Vendors, 2011

Global DRAM and NAND Market Size, 2008-2016E

CAPEX of DRAM Industry, 2000-2013

Global DRAM Shipments, 2000-2013

DRAM Contract Price Change, Jul. 2012-Mar. 2013

DRAM Supply and Demand, Q1 2010-Q4 2014

PC DRAM Supply and Demand, Q1 2010-Q4 2014

DRAM Downstream Market Distribution, 2009-2014

Demand for System Memory, 2001-2013

Ranking of Branded DRAM Vendors by Revenue, Q4 2011

Ranking of Branded DRAM Vendors by Revenue, Q4 2012

Mobile DRAM Market Share, 2009-2011

Mobile DRAM Market Share, 2012

Market Share of Branded NAND Flash Vendors, 2012

NAND Downstream Market Distribution, 2009-2014

GaAs Industry Chain

Main Vendors in GaAs Industry Chain

Ranking of Global GaAs Vendors by Revenue, 2011-2012

Global Installed Fab Capacity by Minimum Geometry, Dec. 2012

Global Installed Fab Capacity by Product Type, Dec. 2012

Global 12-Inch Wafer Capacity, 2011

Global 12-Inch Wafer Capacity, 2013

Global 12-Inch Fab Capacity by Region, 1999-2012

Fab Expenditure by Product, Q4 2011-Q4 2012

Global Installed Wafer Capacity by Product, Q1 2010-Q4 2013

Global Wafer Equipment Spending by Region, 2010-2012

Ranking of World Foundries by Sales, 2005-2012

Operating Margin of the World’s Leading Foundries, 2005-2012

Ranking of the World’s Top 30 MEMS Vendors by Revenue, 2011

Ranking of the World’s Top 20 MEMS Foundries, 2012

China Foundry Sales, 2011

Ranking of the World’s Top 25 IC Design Companies, 2011

Average IC Cost per Phone, 2008-2016

Global Mobile Phone Shipments, 2007-2014

Global CDMA/WCDMA Mobile Phone Shipments by Region, 2010-2013

Quarterly Shipments of the World’s Top Mobile Phone Brands, 2010-2011

Shipments of the World’s Leading Mobile Phone Vendors, 2011-2012

Global Smartphone Operating System Distribution, Q4 2012

Shipments of China’s Leading Smartphone Vendors, 2011-2012

Global PC CPU/GPU Shipments, 2008-2013

Output of Leading Tablet PC Vendors, 2012 vs. 2013

Southeast Asia Fab Equipment Spending by Product Type, 2012-2014

Southeast Asia Capacity by Product, 2011-2014

Global Wafer Equipment Investment Scale, 2007-2016

Global WLP Equipment Spending, 2011-2016

Global Die Packaging Equipment Spending, 2011-2016

Global Automated Testing Equipment Spending, 2011-2016

CAPEX of the World’s Top 10 Semiconductor Vendors, 2011-2012

CAPEX of the World’s Top 10 Semiconductor Vendors, 2013

Global Semiconductor Materials Market by Region, 2010-2013

Global Semiconductor Back-end Equipment Spending by Region, 2010-2012

OSAT Market Size, 2006-2014

Distribution of Global IC Package Type Shipments, 2007

Distribution of Global IC Package Type Shipments, 2010

Distribution of Global IC Package Type Shipments, 2012

Distribution of Global IC Package Type Shipments, 2016

Global Packaging & Testing Market by Technology, 2007 vs. 2011 vs. 2015

Global OSAT Output Value by Region, 2012

Global OSAT Output Value by Region, 2014

Revenue of Taiwan Packaging & Testing Industry, 2007-2011

WLCSP Market Size, 2010-2016

WLCSP Shipments by Application, 2010-2016

Mobile Phone CPU/GPU Package Roadmap

FC Packaging Downstream Market Distribution, 2012

FC-BGA Technology Trends, 2002-2019

Revenue and Operating Margin of the World’s Top 24 Packaging & Testing Vendors, 2008-2012

Organizational Structure of ASE

Revenue and Gross Margin of ASE, 2005-2013

Revenue of ASE by Business, 2010-2012

Copper Wire Bonding Revenue of ASE, Q1 2010-Q4 2011

Copper Wire Bonding Conversion Rate of ASE, Q1 2010-Q4 2011

Copper Wire Bonding Revenue of ASE by Region, Q1 2010-Q4 2011

Copper Wire Bonding Revenue of ASE by Client, Q1 2010-Q4 2011

Revenue and Gross Margin of ASE Packaging, Q1 2010-Q1 2013

Revenue of ASE Packaging by Type, Q1 2011-Q1 2013

Revenue and Gross Margin of ASE Tests, Q1 2010-Q1 2013

Revenue of ASE Tests by Business, Q1 2010-Q1 2012

Revenue, Gross Margin and Operating Margin of ASE Material, Q1 2010-Q1 2013

CAPEX and EBITDA of ASE, Q1 2010-Q1 2013

ASE’s Top 10 Clients, Q1 2012

Revenue of ASE by Application, Q1 2013

ASE Presence in China

Package Type of ASE Shanghai

Revenue of ASE Shanghai, 2004-2011

Revenue, Gross Margin and Operating Margin of Amkor, 2005-2011

Revenue of Amkor by Package Type, 2007-2012

Revenue of Amkor by Package Type, Q4 2008-Q4 2012

Shipments of Amkor by Package Type, Q4 2008-Q4 2012

CSP Revenue of Amkor by Application, 2011

BGA Package Revenue of Amkor by Application, 2011

Leadframe Package Revenue of Amkor by Application, Q3 2011

Revenue and Shipments of Amkor by Region, Q3 2011

Revenue and Shipments of Amkor by Region, 2012

Capacity Utilization of Amkor’s Packaging Business, Q1 2008-Q1 2013

Revenue of Amkor by Application, Q1 2011-Q1 2013

Cost Structure of Amkor, 2011-2012

Organizational Structure of SPIL

Revenue, Gross Margin and Operating Margin of SPIL, 2003-2013

Monthly Revenue and Growth of SPIL, Mar. 2011-Mar. 2013

Revenue of SPIL by Region, 2005-Q4 2012

Revenue of SPIL by Application, 2005-Q4 2012

Revenue of SPIL by Business, 2005-Q4 2012

Capacity of SPIL, Q1 2006 vs. Q2-Q3 2007 vs. Q3-Q4 2011

Copper/Ag Alloy Revenue Quarterly, Q3 2011-Q4 2012

Revenue and Gross Margin of STATS ChipPAC, 2004-2013

Revenue of STATS ChipPAC by Package Type, 2006-Q1 2012

Revenue of STATS ChipPAC by Application, 2006-Q1 2013

Revenue of STATS ChipPAC by Region, 2006-2013

Revenue and Operating Margin of PTI, 2006-2013

Monthly Revenue and Growth Rate of PTI, Mar. 2011-Mar. 2013

PTI Factories

TSV Solutions of PTI

Revenue of PTI by Business, Q4 2012

Revenue of PTI by Product, Q4 2012

Revenue, Gross Margin and Operating Margin of Greatek, 2005-2013

Revenue of Greatek by Technological Type, 2007-2010

Monthly Revenue and Growth Rate of Greatek, Mar. 2011-Mar. 2013

Revenue and Gross Margin of ChipMOS, 2003-2013

Revenue of ChipMOS by Business, 2010-2012

Revenue of ChipMOS by Product, 2010-2012

Utilization Rate and EBITDA Margin of ChipMOS, 2009-2012

Cash Flow and CAPEX of ChipMOS, 2009-2012

Revenue of ChipMOS by Client, 2011

Revenue of ChipMOS by Region, 2006-2011

Revenue and Gross Margin of KYEC, 2002-2013

Monthly Revenue of KYEC, Mar. 2011-Mar. 2013

KYEC Plants

KYEC Testing Platforms

Revenue and EBITDA of Unisem, 2006-2013

Revenue and EBITDA of Unisem, Q1 2010-Q4 2012

Revenue of Unisem by Product, 2012

Revenue of Unisem by Market, 2012

Organizational Structure of Formosa Plastics Group

Organizational Structure of FATC

Revenue and Operating Margin of FATC, 2006-2013

Monthly Revenue of FATC, Mar. 2011-Mar. 2012

Revenue and Operating Margin of JECT, 2006-2013

Output and Sales Volume of JECT, 2011-2012

Testing Cost Structure of JECT, 2011-2012

Package Cost Structure of JECT, 2011-2012

JCET ROADMAP

Revenue of JCET by Region, 2011

Revenue and Operating Margin of LINGSEN, 2007-2013

Monthly Revenue of LINGSEN, Mar. 2011-Mar. 2013

Revenue and Growth Rate of Nantong Fujitsu Microelectronics, 2006-2011

Net Income and Growth Rate of Nantong Fujitsu Microelectronics, 2006-2011

Quarterly Revenue and Growth Rate of Nantong Fujitsu Microelectronics, 2006-2011

Quarterly Net Income and Growth Rate of Nantong Fujitsu Microelectronics, 2006-2011

Quarterly Gross Margin of Nantong Fujitsu Microelectronics, 2006-2011

Quarterly A, S, R&D of Nantong Fujitsu Microelectronics, 2006-2011

Revenue and Operating Margin of Walton Advanced Engineering, 2007-2013

Monthly Revenue and Growth Rate of Walton Advanced Engineering, Mar. 2011-Mar. 2013

Revenue and Operating Margin of Chipbond, 2006-2013

Monthly Revenue and Growth Rate of Chipbond, Mar. 2011-Mar. 2013

Revenue of Chipbond by Business, 2012

Revenue of Chipbond by Product, Q4 2009-Q1 2012

Revenue of Chipbond by Market, 2012

Organizational Structure of J-DEVICES

Revenue and PBT of MPI, FY2007-FY2013

Revenue of MPI by Region

Revenue of Carsem by Product, Q1 2011-Q1 2012

Organizational Structure of STS Semiconductor

Revenue and Operating Margin of STS Semiconductor, 2006-2013

Revenue of STS Semiconductor by Product, Q1 2012-Q4 2013

Shareholder Structure of Signetics

Revenue and Operating Margin of Signetics, 2007-2013

Capacity Utilization and Operating Margin of Signetics, Q1 2010-Q4 2012

Revenue of Signetics by Product, 2011

Revenue of Signetics by Client, 2011

Revenue of Signetics by Technology, Q1 2012-Q4 2013

Revenue and Operating Margin of Hana Micron, 2006-2013

Revenue of Hana Micron by Client, 2011

Revenue of Hana Micron by Market, Q1 2012-Q4 2013

Revenue and Operating Margin of Nepes, 2007-2013

Quarterly Revenue and Operating Margin of Nepes, 2012-2013

Quarterly Revenue of Nepes by Division, 2012-2013

Revenue and Operating Margin of Tian Shui Hua Tian Technology, 2006-2013

如果这份报告不能满足您的要求,我们还可以为您定制报告,请 留言说明您的详细需求。

|