《2018 ADAS与自动驾驶产业链研究——低速自动驾驶产业篇》共190页。该报告主要包含以下内容:

低速自动驾驶产业概述

低速自动驾驶市场综述

国外低速自动驾驶厂商研究

国内低速自动驾驶厂商研究

无人配送车市场及厂商研究

无人作业车市场及厂商研究

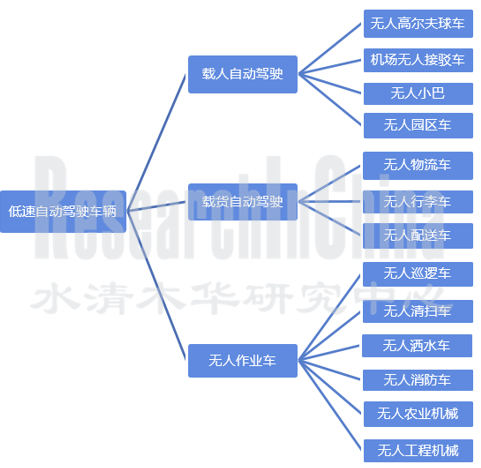

本报告定义的低速自动驾驶车,是指在固定路线道路上或者封闭区域内,以低于30公里/小时的速度运行的自动驾驶车辆。

根据当前市场上出现的各种低速自动驾驶车辆,佐思产研将它们分为载人自动驾驶、载货自动驾驶和无人作业车三大类。

前的自动驾驶技术而言,实现城市复杂道路自动驾驶还为时过早。但在相对封闭的环境或者是有固定路线的道路上实施低速自动驾驶,目前已有较为成熟的技术和方案。部分厂家如Navya已经开始投入商业化应用,其无人驾驶小巴AUTONOM SHUTTLE产量已经突破100辆,并销售至超过16个国家。

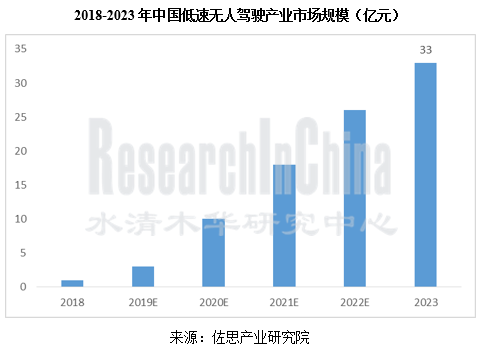

低速自动驾驶车市场虽然刚刚起步,但市场空间非常大,同时中国用户普遍对于新事物接受度比较高,所以发展速度也将快于国外市场。从无人配送车市场起步,中国低速自动驾驶车市场将实现快速增长,保守预计,到2023年该市场规模将达到33亿元。

拥有全世界最大的电子商务市场和最便捷的快递网络,以及人工成本的快速上升,无人配送车市场将是中国低速自动驾驶市场的起爆点。目前多达数十家公司开始切入不同场景的无人配送,包括医院、园区、快递、送餐等。本报告只关注室外无人配送的企业。

人作业车领域,最活跃的是无人农业机械市场,有至少十多家企业投身其中。

ADAS and Autonomous Driving Industry Chain Report 2018 – Low-speed Autonomous Vehicle, 190 pages, focuses on the followings:

Overview of low-speed autonomous driving industry;

Overview of low-speed autonomous driving market;

Foreign low-speed autonomous driving enterprises;

Chinese low-speed autonomous driving enterprises;

Driverless delivery vehicle market and enterprises;

Driverless Working Vehicle Market and Enterprises

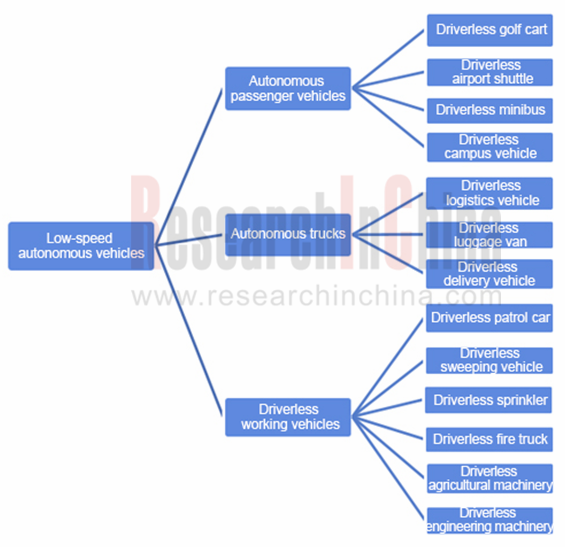

The low-speed autonomous vehicle is defined in the report as the autonomous cars that run at below 30km/h on fixed routes or in enclosed areas.

ResearchInChina divides low-speed autonomous vehicles on the market into three categories: autonomous passenger vehicle, autonomous truck, and driverless working vehicle.

It’s too early for existing autonomous driving technology to enable autonomous driving on complex urban roads. But there are more mature technologies and solutions for low-speed autonomous driving in relatively enclosed areas or on fixed routes. Some enterprises like Navya have put it into commercial application. Navya has produced more than 100 driverless minibuses- AUTONOM SHUTTLE and sold them to more than 16 countries.

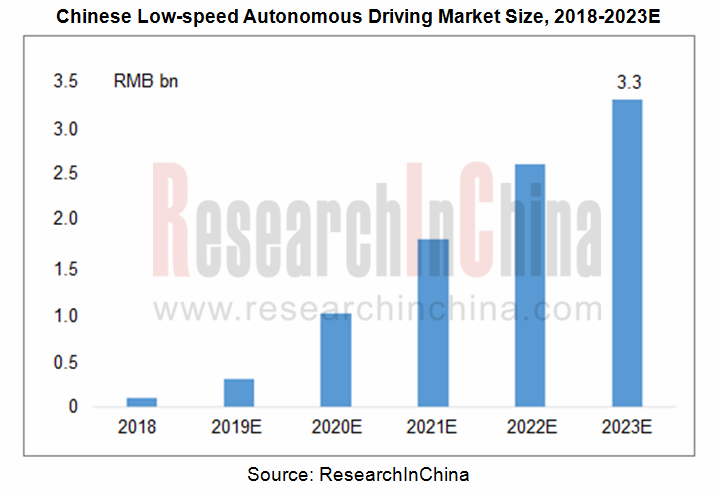

Despite a late starter, China boasts a huge market for low-speed autonomous vehicles. Meanwhile, Chinese users are more receptive to new things. These factors will make the Chinese market develop faster than foreign ones. Beginning with driverless delivery vehicles, the Chinese low-speed autonomous vehicle market will expand rapidly, hitting an estimated RMB3.3 billion conservatively by 2023.

As China is home to the world’s largest E-commerce market and most convenient express delivery network as well as the rapidly rising labor costs, the driverless delivery vehicle market will be a tipping point of the Chinese low-speed autonomous driving market. Dozens of companies have made a foray into unmanned delivery under different scenarios, including hospital, campus, express delivery and meal delivery service. The report here focuses on only outdoor autonomous delivery enterprises.

The driverless agricultural machinery market, the most active segment in driverless working vehicle field, has attracted more than a dozen businesses.

第一章 低速自动驾驶产业简介

1.1 低速自动驾驶车的定义

1.2 低速自动驾驶车辆分类

1.3 无人小巴的运营模式

1.4 低速自动驾驶的三大难点

1.5 国内外数十家厂商进入

1.6 美国各地正在进行各种低速无人车试运营

第二章 低速自动驾驶市场综述

2.1 2018-2025全球无人小巴市场规模-数量

2.2 2018-2025全球无人小巴市场规模-金额

2.3 无人小巴细分市场:私人交通

2.4 无人小巴细分市场:公共交通

2.5 竞争格局:现阶段主要竞争者

2.6 竞争格局:潜在竞争者

2.7 中国低速自动驾驶车市场规模预计

2.8 中国无人小巴市场规模预计

2.9 自动驾驶落地路径

第三章 国外低速自动驾驶厂商研究

3.1 Easy Mile

3.1.1 Easy Mile 主要运行项目

3.2 Navya

3.2.1 发展历程

3.2.2 AUTONOM SHUTTLE

3.2.3 AUTONOM Cab

3.2.4 经营情况

3.2.5 价值链环节主要合作伙伴

3.3 Local Motors

3.3.1 测试项目

3.4 Auro Robotics

3.5 May Mobility

3.6 Einride

3.7 2getthere

3.7.1 主要项目

3.8 BestMile

3.8.1 自动驾驶移动服务平台

3.8.2 主要客户及项目

3.9 TARDEC

3.9.1 无人车实验室

3.9.2 TARDEC作战系统项目

3.10 SB Drive

3.10.1 发展历程

3.11 Auto X

3.11.1 主要产品

3.11.2 低速自动驾驶产品

3.12 ohmio

3.12.1 主要产品

3.12.2 最新发展

3.13 Oxbotica

3.13.1 CargoPod

3.13.2 Driven项目

3.14 e.GO Mobile

第四章 国内低速自动驾驶厂商研究

4.1 北京智行者

4.1.1 公司简介

4.1.2 发展历程

4.1.3 低速自动驾驶方案

4.1.4 蜗必达

4.1.5 开发园区无人配送物流车遇到的挑战

4.1.6 产品技术架构

4.2 驭势科技

4.2.1 产品及技术

4.2.2 无人驾驶行李物流车

4.3 青飞智能

4.3.1 主要技术

4.3.2 产品路线

4.3.3 产品测试

4.3.4 与上海交大联合研制无人驾驶小巴

4.4 天隼图像

4.4.1 主要产品

4.4.2 自动驾驶系统构成

4.4.3 其他自动驾驶衍生车型

4.5 诗航智能

4.5.1 战略规划

4.6 易成自动驾驶

4.6.1 业务进展

4.6.2 主要产品

4.6.3 主要项目落地情况

4.6.4 主要技术

4.7 海高汽车

4.7.1 低成本无人清扫车

4.7.2 发展规划

4.8 深兰科技

4.8.1 主要产品

4.8.2 芭提雅自动驾驶车

4.9 百度阿波龙项目

4.9.1 阿波龙简介

4.9.2“MiniBus-自动接驳小巴”自动驾驶套件

4.9.3“MicroCar-无人作业小车”自动驾驶套件

4.9.4 车队管理平台

4.9.5 适用场景

4.10 智尊保

第五章 无人配送车市场及厂商

5.1 无人配送车市场

5.1.1 无人配送车发展现状和趋势

5.1.2 无人配送车发展的难点

5.1.3 无人配送车市场主要企业及对比

5.2 苏宁物流

5.2.1 无人驾驶产品

5.2.2 加入Apollo联盟

5.3 美团

5.3.1 业务发展历程及规划

5.3.2 美团加入BDD

5.3.3 美团发布无人配送开放平台

5.4 京东X事业部

5.4.1 无人车发展历程

5.4.2 主要项目

5.4.3 京东无人车落户长沙

5.5 菜鸟网络

5.5.1 产品线

5.5.2 主要功能

5.6 Nuro.ai

5.7 Starship

5.8 武汉小狮科技

5.8.1 主要产品技术

5.8.2 无人物流配送车的运营

5.9 新石器

5.9.1 发展历程

5.9.2 硬件产品

5.9.3 软件技术

5.9.4 工厂

5.10 Auto X

5.10.1 研发情况

5.10.2 低速无人送货车

5.11 Marble

5.12 普渡科技

5.13 高仙机器人

第六章 无人作业车市场及厂商

6.1 无人作业车的发展趋势

6.1.1 农机无人驾驶的行业动向

6.1.2 工程机械无人驾驶的发展动向

6.2 沃尔沃

6.3 小松

6.4 中联重机

6.4.1 智慧农业和自动驾驶

6.4.2 农机自动驾驶主要技术

6.4.3无人驾驶谷物收割机

6.5 踏歌智行

6.5.1 发展历程

6.5.2 踏歌自动驾驶机器人应用场景

6.5.3 在测试领域的应用

6.5.4 在工程机械领域的应用

6.5.5 在矿用车的应用

6.6 中创博远

6.7 雷沃重工

6.8 国机重工

6.9 中大机械

6.10 三一重机

6.11 合众思壮

6.12 酷哇科技

1 Low-speed Autonomous Driving Industry

1.1 Definition of Low-speed Autonomous Vehicle

1.2 Classification of Low-speed Autonomous Vehicle

1.3 Business Model of Driverless Minibus

1.4 Three Difficulties for Low-speed Autonomous Driving

1.5 Dozens of Entrants at Home and Abroad

1.6 Trial Operation of Low-speed Autonomous Vehicle in the United States

2 Low-speed Autonomous Driving Market

2.1 Global Driverless Minibus Market Size during 2018-2025 - Quantity

2.2 Global Driverless Minibus Market Size during 2018-2025 - Value

2.3 Driverless Minibus Market Segment: Private Traffic

2.4 Driverless Minibus Market Segment: Public Transport

2.5 Competition: Major Contenders at Present

2.6 Competition: Potential Competitors

2.7 Forecast of Low-speed Autonomous Vehicle Market Size in China

2.8 Forecast of Driverless Minibus Market Size in China

2.9 Grounding Paths for Autonomous Driving

3 Foreign Companies in Low-speed Autonomous Driving

3.1 Easy Mile

3.1.1 Major Projects in Service

3.2 Navya

3.2.1 Development Course

3.2.2 AUTONOM SHUTTLE

3.2.3 AUTONOM Cab

3.2.4 Operation

3.2.5 Major Partners in Value Chains

3.3 Local Motors

3.3.1 Testing Projects

3.4 Auro Robotics

3.5 May Mobility

3.6 Einride

3.7 2getthere

3.7.1 Major Projects

3.8 BestMile

3.8.1 Mobility Service Platform

3.8.2 Major Customers and Projects

3.9 TARDEC

3.9.1 Self-driving Car Laboratory

3.9.2 TARDEC Combat System Project

3.10 SB Drive

3.10.1 Development Course

3.11 Auto X

3.11.1 Major Products

3.11.2 Low-speed Autonomous Driving Products

3.12 ohmio

3.12.1 Major Products

3.12.2 Latest Developments

3.13 Oxbotica

3.13.1 CargoPod

3.13.2 Driven Project

3.14 e.GO Mobile

4 Chinese Companies in Low-speed Autonomous Driving

4.1 IDRIVERPLUS

4.1.1 Profile

4.1.2 Development Course

4.1.3 Low-speed Autonomous Driving Solutions

4.1.4 WOBIDA(Ω)

4.1.5 Challenges to Driverless Delivery Vehicle in Development Parks

4.1.6 Product Technology Architecture

4.2 UISEE

4.2.1 Products & Technologies

4.2.2 Autonomous Luggage Logistics Vehicle

4.3 MAGRIDE

4.3.1 Key Technologies

4.3.2 Product Roadmap

4.3.3 Product Testing

4.3.4 Driverless Shuttle Co-developed with Shanghai Jiao Tong University

4.4 FALCON

4.4.1 Major Products

4.4.2 Autonomous Driving System Composition

4.4.3 Other Autonomous Derivative Models

4.5 Navibook

4.5.1 Strategic Planning

4.6 Shenzhen Echiev Autonomous Driving Technology

4.6.1 Business Progress

4.6.2 Major Products

4.6.3 Implementation of Major Projects

4.6.4 Key Technologies

4.7 HiGo Automotive

4.7.1 Low-cost Driverless Sweeper

4.7.2 Development Planning

4.8 DeepBlue Technology

4.8.1 Major Products

4.8.2 “Batiya” Autonomous Vehicle

4.9 Baidu Apolong Project

4.9.1 Introduction to Apolong

4.9.2 “MiniBus” Autonomous Driving Suite

4.9.3 “MicroCar”Autonomous Driving Suite

4.9.4 Fleet Management Platform

4.9.5 Applicable Scenarios

4.10 Zoominbot

5 Driverless Delivery Vehicle Market and Manufacturers

5.1 Driverless Delivery Vehicle Market

5.1.1 Development Status Quo and Trend of Driverless Delivery Vehicle

5.1.2 Difficulties in the Development of Driverless Delivery Vehicle

5.1.3 Key Plays in Driverless Delivery Vehicle Market and Comparisons

5.2 SUNING

5.2.1 Self-driving Products

5.2.2 Joining Apollo Alliance

5.3 Meituan

5.3.1 Business Development Course and Planning

5.3.2 Joining BDD

5.3.3 Meituan Released Its Driverless Delivery Open Platform

5.4 JD X Business Division

5.4.1 Development Course of Self-driving Car

5.4.2 Main Projects

5.4.3 JD Self-driving Car Settled in Changsha

5.5 Cainiao

5.5.1 Product Line

5.5.2 Key Functions

5.6 Nuro.ai

5.7 Starship

5.8 Aisimba

5.8.1 Product Technologies

5.8.2 Operation of Driverless Delivery Vehicle

5.9 Neolix

5.9.1 Development Course

5.9.2 Hardware Products

5.9.3 Software Technologies

5.9.4 Plants

5.10 Auto X

5.10.1 R&D

5.10.2 Low-speed Driverless Delivery Vehicle

5.11 Marble

5.12 Pudu Tech

5.13 Gaussian Robotics

6 Driverless Working Vehicle Market and Manufacturers

6.1 Development Trend of Driverless Working Vehicle

6.1.1 Development of Autonomous Driving in Agricultural Machinery

6.1.2 Development of Autonomous Driving in Construction Machinery

6.2 Volvo

6.3 Komatsu

6.4 Zoomlion Heavy Machinery

6.4.1 Intelligent Agriculture and Autonomous Driving

6.4.2 Autonomous Driving Technologies for Agricultural Machinery

6.4.3 Self-driving Grain Harvester

6.5 i-Tage Technology

6.5.1 Development Course

6.5.2 Applied Scenarios of i-Tage Autonomous Robot

6.5.3 Application in Testing Field

6.5.4 Application in Construction Machinery

6.5.5 Application in Mining Vehicle

6.6 Beijing Zhongchuang Byfarming Intelligent Technology

6.7 Lovol Heavy Industry

6.8 China SINOMACH Heavy Industry Corporation

6.9 Shaanxi Jointark Machinery Group

6.10 Sany Heavy Industry

6.11 UniStrong

6.12 COWAROBOT